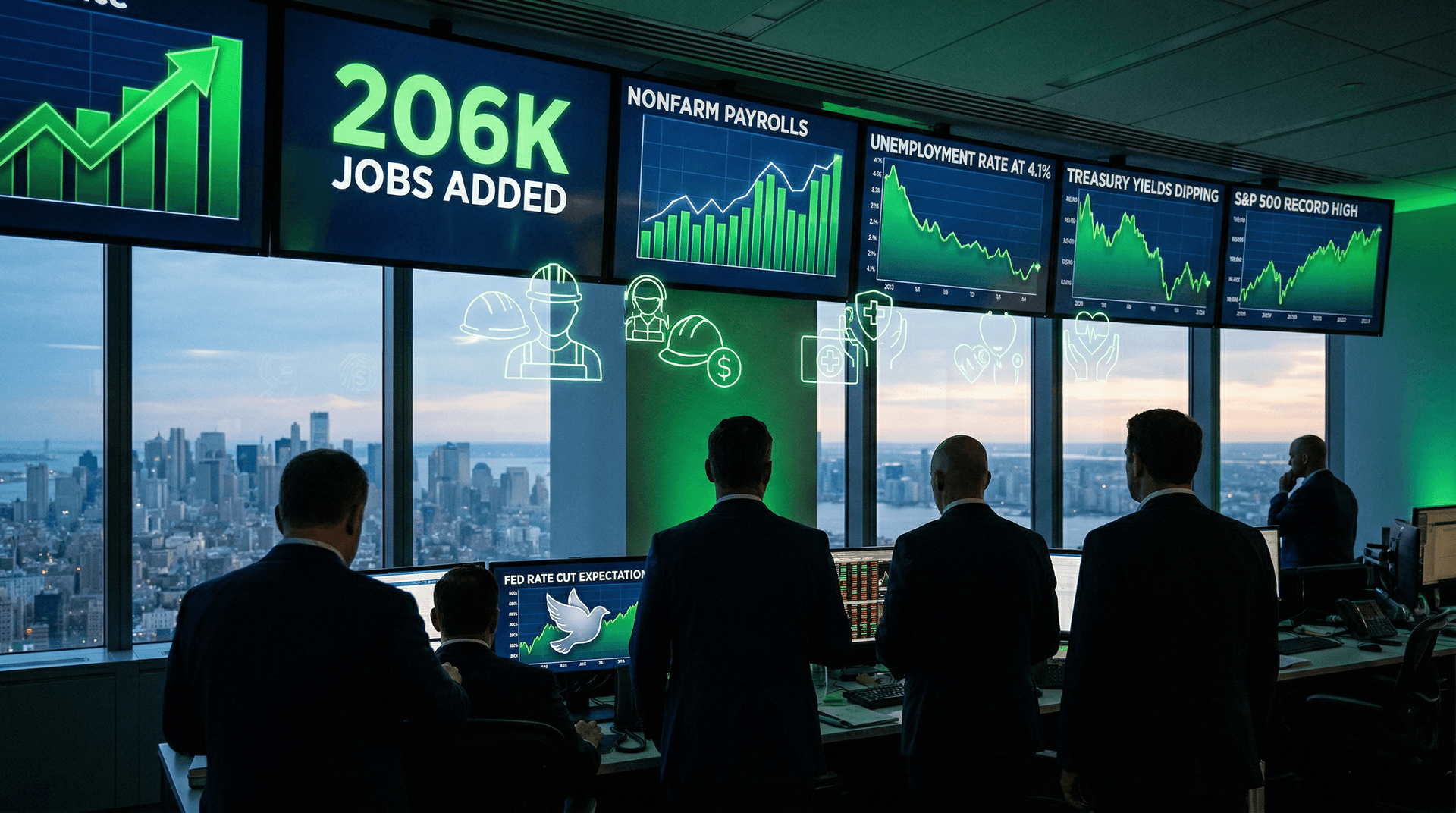

On July 5, 2024, the US Bureau of Labor Statistics (BLS) released its closely watched June nonfarm payrolls report, revealing a labor market that continues to defy recession fears but shows unmistakable signs of deceleration. Nonfarm payrolls increased by 206,000, surpassing economist consensus estimates of around 190,000. However, this headline figure masks deeper nuances: significant downward revisions to prior months and a slight uptick in the unemployment rate to 4.1% from 4.0%. As markets digest these data points, the report reinforces the narrative of a 'soft landing'—economic growth without a sharp downturn—but raises questions about the Federal Reserve's path forward.

Breaking Down the Numbers

The 206,000 jobs added represent a slowdown from the revised 186,000 in May (down 86,000 from the initial 272,000 estimate) and 165,000 in April (down 8,000). Government hiring drove much of June's gains, with 70,000 jobs in local government education and 39,000 in state government. Private sector payrolls added 147,000, led by healthcare (+22,000), leisure and hospitality (+19,000), and manufacturing (+3,000)—a rare bright spot amid broader industrial weakness.

Unemployment rose to 4.1%, with the labor force participation rate edging up to 62.6%. Broader measures like U-6 (underemployment) held steady at 7.4%. Wage growth moderated slightly, with average hourly earnings up 0.2% monthly and 3.9% annually—below May's 4.1% but still above the Fed's 2% inflation target, fueling ongoing inflation debates.

These figures align with other indicators: The ADP private payrolls report on July 3 showed just 150,000 jobs added, and the ISM manufacturing PMI remained in contraction territory at 48.5 for June. Yet services held firm, with ISM services PMI at 48.8, indicating resilience in consumer-driven sectors.

Market Reactions and Fed Watch

Wall Street responded bullishly. The S&P 500 climbed 0.8% to a record high on July 5, while the Nasdaq surged 1.1%. The 10-year Treasury yield dipped below 4.3%, reflecting bets on imminent rate cuts. CME FedWatch Tool odds for a September 25-basis-point cut jumped to 75% from 60% pre-report, with markets pricing in 65 basis points of easing by year-end.

Fed Chair Jerome Powell has emphasized data-dependence, and this report provides it: cooling job growth reduces overheating risks without tipping into contraction. However, persistent wage pressures and sticky services inflation (PCE core at 2.6% in May) complicate the pivot. Upcoming CPI data on July 11 will be pivotal, but the jobs print tilts the balance toward easing.

Broader Macro Implications

This data arrives amid a complex macroeconomic backdrop. US GDP grew 1.4% annualized in Q1 2024, with Q2 estimates around 2.0% from the Atlanta Fed GDPNow tracker. Consumer spending remains robust—retail sales up 0.2% in very preliminary June figures—but delinquencies are rising in credit cards and auto loans, per New York Fed reports.

Globally, the US stands as an outlier. China's factory activity contracted for the third month in June (Caixin PMI 49.4), Europe's ECB cut rates on June 6 amid stagnant growth, and Japan's yen weakness persists despite BoJ hikes. The dollar index (DXY) softened post-jobs data, aiding emerging markets but pressuring US exporters.

Geopolitical Crosscurrents

Timing is everything. The report coincides with political turbulence: UK voters delivered a Labour landslide on July 4, ousting Conservatives after 14 years. Markets welcomed Keir Starmer's stability pledge, with FTSE 100 up 0.9% on July 5. In France, the June 30 legislative first-round shock—left-wing alliance topping Macron's centrists—has markets on edge for the July 7 runoff, with CAC 40 volatility spiking.

US elections loom large. Post-debate (June 27), President Biden's support waned, boosting Trump odds. A Republican sweep could mean tax cuts and deregulation, supercharging growth but inflating deficits. Labor market softness plays into narratives: Trump campaigns on 'Bidenomics failure,' while Democrats highlight resilience.

Risks and Forward Outlook

Bullish voices, including Goldman Sachs (raising recession odds to 30%), see soft landing intact. Bears point to revisions averaging -20,000 monthly, Sahm Rule flashing mild recession risk (unemployment rise 0.5% over 12 months), and inverted yield curve persistence.

Corporate America signals caution: Layoff announcements hit 75,000 in June (Challenger Gray), led by tech (Microsoft, Intel cuts). AI investments promise productivity gains, but short-term disruptions loom.

Policy divergence persists. Fed cuts contrast with hawkish ECB/BoE tones post-UK vote. Geopolitical flashpoints—Ukraine aid debates, Middle East tensions—add oil price volatility (WTI ~$83/bbl).

Investment Strategies

- Equates: Favor cyclicals (financials, industrials) over mega-caps; small-caps (Russell 2000 +2.5% post-report).

- Fixed Income: Lock in yields; expect 10-year to 4.0% by September.

- Commodities: Gold rallies on rate cut bets (+1.2% to $2,360/oz).

- Global: UK gilts attractive; avoid French bonds pre-election.

In sum, June's jobs report underscores a labor market in controlled slowdown—goldilocks for now. Yet reversals, geopolitics, and Fed missteps pose tail risks. Investors should brace for volatility as data shapes destiny in this election year.

Word count: 912