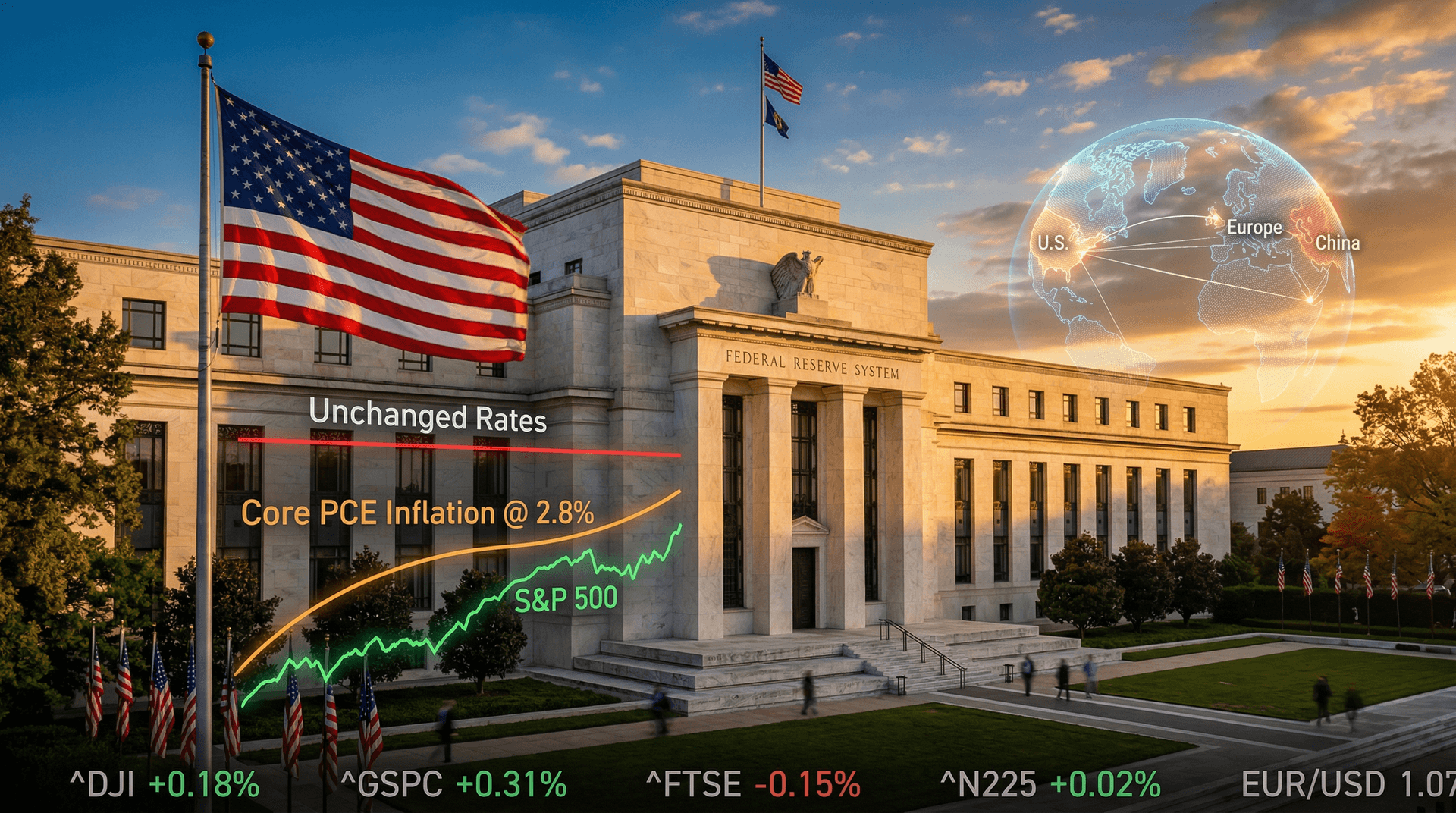

The Federal Open Market Committee (FOMC) convened on May 1, 2024, delivering a widely anticipated decision to keep the federal funds rate unchanged at 5.25-5.50%. This marks the seventh consecutive meeting without a rate adjustment, underscoring the U.S. central bank's hawkish tilt in the face of stubbornly high inflation. Federal Reserve Chair Jerome Powell, in his post-meeting press conference, reiterated that policymakers are well-positioned to wait for clearer evidence that inflation is sustainably moving toward the 2% target before considering any easing.

Background: From Aggressive Hiking to Strategic Pause

The Fed's current policy stance is the culmination of a rapid tightening cycle that began in March 2022. Over that period, the central bank hiked rates by 525 basis points to combat inflation that peaked at 9.1% in June 2022. Recent data has shown progress: Core PCE inflation, the Fed's preferred gauge, eased to 2.8% in March 2024 from highs above 5%. However, first-quarter GDP estimates and persistent shelter costs have tempered optimism.

The Summary of Economic Projections (SEP) released alongside the statement painted a slightly more hawkish picture than the March update. Median projections now foresee only one 25-basis-point rate cut by year-end 2024, down from three previously anticipated. GDP growth was revised down to 1.7% for 2024, unemployment ticked up to 3.9%, and core PCE inflation held steady at 2.6%. This dot plot shift reflects a consensus that the disinflation process remains incomplete.

Powell's remarks were measured yet firm. "We did not expect to be in this situation," he noted, referring to the need for restrictive policy longer than initially thought. He highlighted upside risks to inflation from supply chain disruptions and geopolitical tensions, including the ongoing Russia-Ukraine conflict and Red Sea shipping attacks, which have kept energy and commodity prices elevated.

Immediate Market Reactions

U.S. equity markets absorbed the news with equanimity. The S&P 500 rose 1.3% to close at 5,018.39, buoyed by strong Big Tech earnings in the prior week. The Nasdaq Composite climbed 2.2%, reflecting resilience in growth stocks despite higher-for-longer rate expectations. The 10-year Treasury yield dipped slightly to 4.50% from 4.69%, as investors parsed the SEP's tempered cut outlook.

The dollar index (DXY) strengthened modestly, pressuring emerging market currencies. Gold prices, a traditional inflation hedge, held above $2,300 per ounce. In currency markets, the euro weakened against the dollar, influenced by the European Central Bank's more dovish signals ahead of its own June meeting.

Macroeconomic Implications

This decision reinforces a soft-landing narrative, where the Fed aims to curb inflation without triggering recession. Labor market data supports this: April's nonfarm payrolls preview (released later but anticipated) showed resilience with 3.8% unemployment and steady wage growth. However, leading indicators like the ISM Manufacturing PMI at 49.0 signal contraction risks.

Consumer spending, which drives 70% of U.S. GDP, faces headwinds from elevated borrowing costs. Mortgage rates near 7% have stalled housing activity, a key inflation driver via shelter costs (40% of CPI). Corporate profit margins, squeezed by input costs, may face further pressure if rates stay high, potentially curbing capex in tech and infrastructure.

Geopolitically, the Fed's caution aligns with global fragmentation. U.S.-China trade tensions persist, with new tariffs on EVs and semiconductors looming under potential policy shifts post-election. Middle East instability sustains oil above $80/barrel, embedding imported inflation. Europe's energy crisis, exacerbated by sanctions on Russian gas, keeps ECB rates higher, reducing policy divergence.

Impact on Technology and Finance Sectors

As a tech journalist, the intersection of monetary policy and innovation is particularly salient. Higher rates discount future cash flows, challenging high-valuation tech giants. Nvidia's recent surge on AI demand notwithstanding, broader semis face inventory gluts. Cloud providers like AWS and Azure see enterprise spend softening amid cost controls.

Fintech and crypto markets, sensitive to liquidity, traded sideways. Bitcoin hovered near $63,000, with spot ETFs inflows slowing. Venture capital fundraising dipped 20% YoY, per PitchBook data, as LPs demand higher hurdles in a 5%+ rate environment.

Banking stocks outperformed, with JPMorgan and Goldman Sachs up 2-3%, betting on net interest income stability. Regional banks, scarred by 2023 failures, benefit from steady rates avoiding deposit flight.

Global Ripples and Policy Divergence

Emerging markets (EMs) brace for capital outflows. Brazil's Selic rate at 10.75% and India's repo at 6.5% reflect catch-up tightening. China's property woes and weak stimulus response pressure the yuan, indirectly supporting U.S. export competitiveness.

In geopolitics, the Fed's stance bolsters the dollar's reserve status, aiding sanction efficacy against Russia and Iran. Yet, it complicates debt servicing for developing nations; IMF warnings of $10 trillion in EM debt highlight risks.

Outlook: Data-Dependent Path Forward

Upcoming data will dictate June's FOMC: April CPI (May 15), retail sales, and Powell's testimony. Markets price a 25% chance of a June cut, per CME FedWatch. If inflation reaccelerates—say, via summer energy spikes—the Fed could hike anew, a scenario Powell deemed unlikely but possible.

Strategically, this pause buys time for fiscal consolidation amid $34 trillion U.S. debt. Tech innovation in AI and renewables could enhance productivity, aiding disinflation. However, regulatory scrutiny on Big Tech monopolies risks stifling growth.

In sum, May 1's decision is a pivot to patience. Markets rally on soft-landing hopes, but macro headwinds—geopolitical strife, fiscal largesse, structural inflation—counsel vigilance. Investors should favor quality over speculation, with diversified portfolios weathering prolonged restriction.

(Word count: 912)