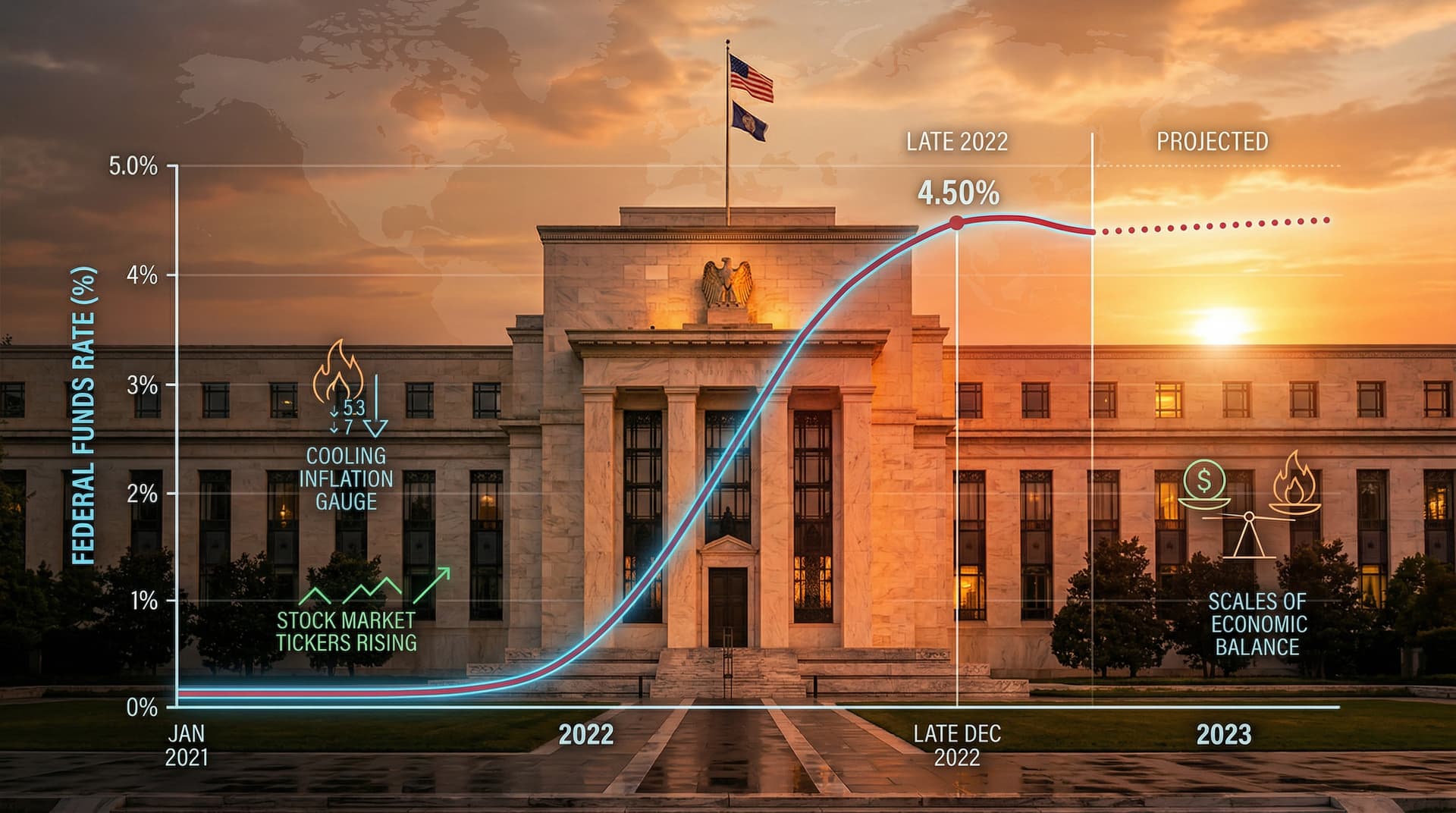

In a widely anticipated move, the US Federal Reserve on December 14 raised its benchmark interest rate by 50 basis points, lifting the federal funds target range to 4.25%-4.50%. This marks the seventh consecutive rate increase since March, but the smallest hike since the aggressive cycle began, signaling a potential pivot toward a more gradual path as inflation shows signs of moderation.

Federal Reserve Chair Jerome Powell, in his post-meeting press conference, struck a cautiously optimistic tone. "Inflation has been moderating in recent months, but remains well above our 2% target," Powell stated. He highlighted the impact of tighter monetary policy on demand, noting that job growth remains robust but wage pressures are easing. The updated Summary of Economic Projections (SEP) revealed Fed officials now expect the policy rate to peak at 5.1% by the end of 2023, down from a prior median of 5.6%, with two additional 50 bps hikes anticipated next year followed by cuts in 2024.

Market Reaction: Relief Rally Across Assets

Markets responded with jubilation. The S&P 500 surged 3.1% on the announcement day, its best single-day gain in months, while the Nasdaq Composite climbed 4.3%, buoyed by tech stocks. The 10-year Treasury yield dipped below 3.8%, reflecting bets on fewer hikes ahead. The US dollar weakened against major currencies, providing some relief to emerging markets battered by prior tightening.

This reaction underscores investor fatigue with the Fed's hawkish stance. Since June's 75 bps mega-hikes, data has improved: CPI cooled to 7.1% year-over-year in November from a 9.1% peak in June, core PCE—the Fed's preferred gauge—hit 5.6% annualized in October. Housing starts and retail sales have softened, validating the policy's bite.

Policy Context: From Shock Hikes to Deliberate Tightening

The Fed's journey began in March with a surprise 25 bps hike amid post-pandemic inflation fueled by supply snarls, stimulus spending, and energy shocks from Russia's invasion of Ukraine. Subsequent 75 bps jolts in June, July, September, and November pushed rates to combat what Powell called a "multidecade high" in prices.

Geopolitics amplified the challenge. Brent crude oscillated above $80 per barrel through much of 2022, with Ukraine war sanctions curbing Russian supply. Europe's energy crisis, including Germany's Nord Stream sabotage in late September, rippled globally, embedding imported inflation. Meanwhile, China's zero-COVID lockdowns disrupted manufacturing, tightening supply chains.

Yet, policy transmission is working. Bank lending standards have tightened, credit card rates top 20%, and mortgage rates near 7% have frozen housing. Unemployment holds at 3.7%, but Powell warned of a possible mild recession if disinflation stalls.

Dot Plot Shift: Decoding the Fed's New Path

The SEP dot plot was the star. Nine of 19 officials now see rates at or below 4.1% by end-2023, versus just four in September—a dovish flip. GDP growth forecasts were trimmed to 1.2% for 2023 from 1.8%, with unemployment rising to 4.6%. Inflation projections eased to 3.5% core PCE by year-end.

Critics argue the Fed lagged, with Minneapolis Fed President Neel Kashkari dissenting for a 75 bps hike. Powell countered that data-dependent decisions prevent over-tightening, invoking the 1970s Volcker era as a cautionary tale of boom-bust cycles.

| Key SEP Updates (Median) | 2022 | 2023 | 2024 | |---------------------------|------|------|------| | Federal Funds Rate | 4.4% | 5.1% | 4.3% | | Core PCE Inflation | 5.5% | 3.5% | 2.4% | | Unemployment Rate | 3.7% | 4.6% | 4.8% | | Real GDP Growth | 1.3% | 1.2% | 1.8% |

Global Ripples: ECB, BoJ, and Emerging Markets

The Fed's move reverberates worldwide. The ECB followed suit on December 15 with a 50 bps hike to 2.5%, citing eurozone inflation at 10.1%. Bank of England added 50 bps to 3.5%. Even the Bank of Japan tweaked its yield curve control on December 20, allowing 10-year JGB yields up to 0.5% amid yen weakness.

Emerging markets sigh relief. India's rupee stabilized, Brazil's real gained, as dollar downside aids debt servicing. But risks persist: if US recession materializes, global demand craters, hitting commodity exporters.

Geopolitically, US policy intersects with national security. The CHIPS Act and Inflation Reduction Act, passed earlier, channel fiscal support toward domestic semiconductors and green tech, countering China. Treasury's G7-coordinated Russian oil price cap at $60/barrel, enforced since December 5, aims to starve Moscow's war chest without spiking prices—though evasion via shadow fleets looms.

2023 Outlook: Balancing Act Amid Uncertainties

Looking ahead, January's CPI and payrolls will set January 31 FOMC tone. Powell pledged vigilance on "headline" inflation from food/energy, but core trends matter most. Recession odds—per Bloomberg at 70%—hinge on consumer spending, 70% of GDP.

Fiscal policy complicates: Congress's lame-duck $1.7 trillion omnibus on December 22 averts shutdown but adds deficit pressure. Biden's student debt forgiveness, partially upheld, injects liquidity.

For investors, bonds regain appeal with yields up, but equities eye earnings. Tech, slammed 30% YTD, rebounds on rate sensitivity. Gold and bitcoin waver as real yields rise.

Broader Implications for Macro Stability

This Fed pivot embodies macro policy's high-stakes chess. Success curbs inflation without crash-landing growth, restoring credibility post-2021 "transitory" missteps. Failure risks stagflation, eroding trust in institutions amid populist surges.

Globally, synchronized tightening tests Bretton Woods II resilience. As US exceptionalism—strong jobs, shale energy—buffers shocks, allies lean on Washington. Yet, multipolarity rises: Saudi-led OPEC+ cuts test dollar hegemony.

In sum, December's hike closes a blistering chapter, opening cautious thaw. Markets price four more hikes to 5.1%, but Powell's "not there yet" mantra prevails. As 2022 ends, policy anchors 2023's narrative—disinflation triumph or hard landing? Data will decide.

Word count: 912