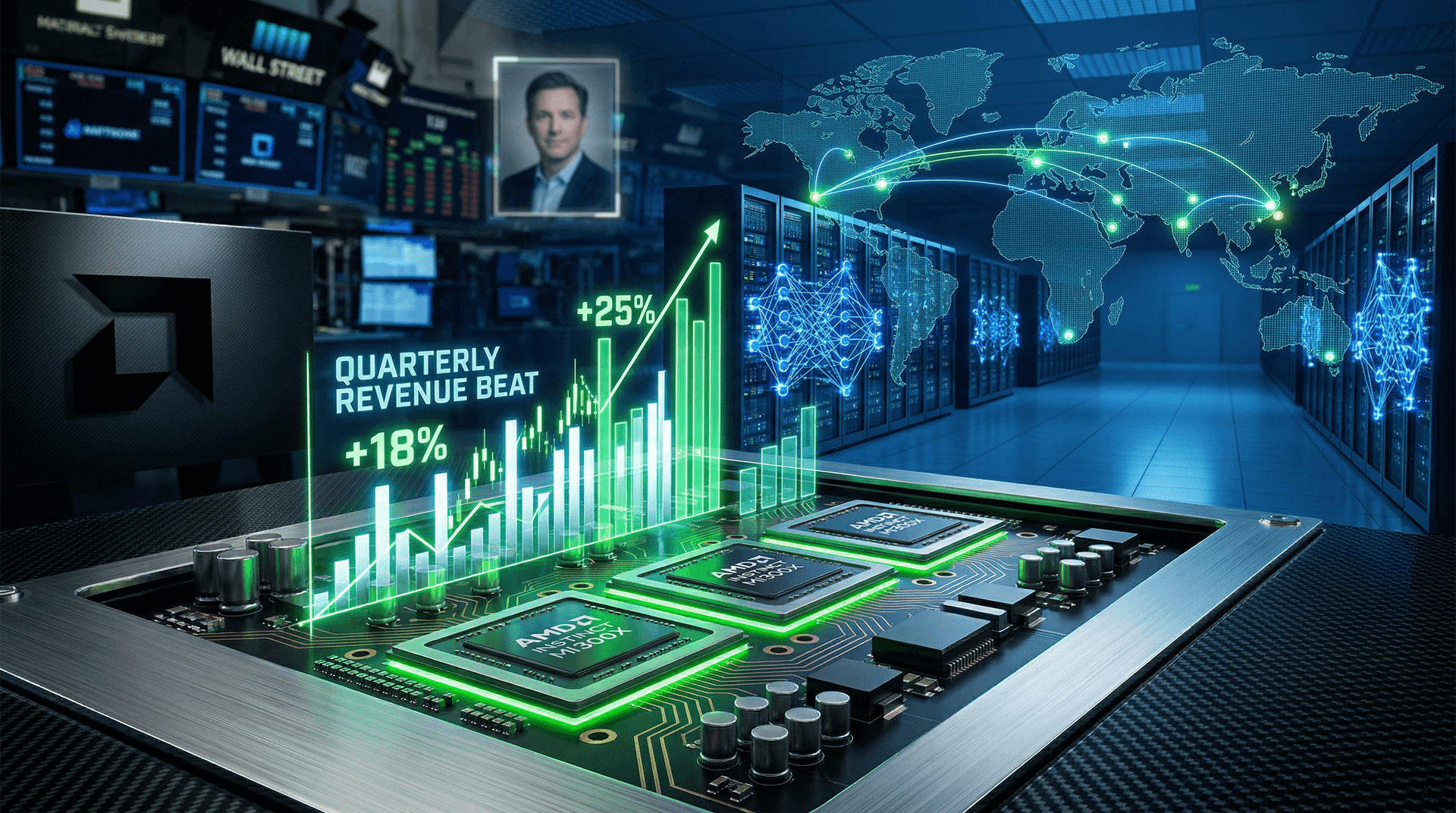

In a testament to the unrelenting hunger for artificial intelligence hardware, Advanced Micro Devices (AMD) reported second-quarter results on August 1 that obliterated Wall Street expectations. Revenue came in at $5.36 billion, surpassing the consensus estimate of $5.08 billion by a wide margin. Adjusted earnings per share hit $0.58, topping forecasts of $0.52. But the real story lay in the data center segment, where revenue rocketed 80% year-over-year to $1.29 billion—almost entirely fueled by sales of AI-optimized GPUs and accelerators.

CEO Lisa Su, in her post-earnings call, painted a vivid picture of the AI revolution reshaping the semiconductor landscape. "We are entering a multi-year AI accelerator cycle," she declared, highlighting the ramp-up of the Instinct MI300X GPU family. These chips, positioned as direct challengers to Nvidia's H100, are already securing design wins with major cloud providers. Su noted that MI300X inference performance crushes competitors, positioning AMD to capture a slice of the burgeoning market for training and running large language models like those powering ChatGPT.

The AI Gold Rush: Hyperscalers Lead the Charge

The earnings reflect a macro tailwind that's hard to overstate: massive capital expenditures from Big Tech. Microsoft, Amazon, Google, and Meta have collectively pledged tens of billions in 2023 for AI infrastructure. Nvidia has been the prime beneficiary, its stock up over 150% year-to-date as of early August, but AMD's results signal that the pie is expanding faster than any single player can consume it.

Data center now accounts for 24% of AMD's total revenue, up from mid-teens levels last year. Client segment (PCs) grew modestly 6% to $1.2 billion, buoyed by Ryzen 7000 series adoption, while gaming dipped 6% to $824 million amid console cycle softness. Embedded revenue held steady at $827 million. Yet, it's the AI ramp that has investors salivating. For Q3, AMD guided $5.3 billion to $5.7 billion in revenue—above the $5.17 billion street view—and raised full-year data center projections to $3.5 billion.

Stock market reaction was swift: shares jumped 6% in after-hours trading on August 1, adding billions to AMD's market cap, now hovering around $150 billion. This comes as Nvidia's dominance—controlling 80-90% of AI GPU market share—faces its first serious broad-based challenge.

Geopolitical Headwinds and Supply Chain Realities

Amid the euphoria, macro and geopolitical risks loom large. The U.S.-China tech decoupling intensified in recent weeks, with the Biden administration's July expansion of export controls on advanced chips to China. AMD, like peers, derives a portion of revenue from the region but has ramped U.S. and allied production. Taiwan Semiconductor Manufacturing Co. (TSMC), which fabs AMD's cutting-edge nodes, remains a chokepoint. Any escalation in Taiwan Strait tensions could ripple through global AI supply chains.

Lisa Su addressed this head-on: "Geopolitical issues are top of mind, but we're diversified." AMD's strategy includes expanding U.S. manufacturing partnerships and qualifying chips for export-compliant customers. Still, China's push for AI self-sufficiency—via homegrown firms like Huawei—poses long-term competitive threats, even as U.S. restrictions curb their access to top-tier silicon.

Macro Implications: A Semiconductor Supercycle?

Zooming out, AMD's beat reinforces the narrative of a semiconductor supercycle driven by AI. Global foundry utilization rates are north of 90%, pricing power is firm, and lead times stretch into 2024. Hyperscalers' AI capex is projected to exceed $100 billion this year, per analysts, spilling over into enterprise and edge AI applications.

Yet, it's not all smooth sailing. Valuations are stretched—AMD trades at 45x forward earnings—and a broader market pullback could clip wings. Inflation data due this week, alongside Fed rate hike odds, adds volatility. Moreover, energy demands of AI data centers strain grids, prompting sustainability debates. Microsoft alone expects AI to double its power needs by 2025.

AMD vs. Nvidia: The Battle Heats Up

Nvidia's CUDA software moat remains formidable, locking in developers. But AMD's open-source ROCm platform is gaining traction, with recent optimizations for MI300. Partnerships with Microsoft (via Azure) and Oracle bolster credibility. Su claims MI300X offers 35% better inference than H100 at similar power envelopes—a bold pitch amid power-constrained data centers.

Wall Street's take: JPMorgan raised its price target to $155, citing AI upside. The firm sees AMD chipping away at Nvidia's share, potentially to 10-15% in coming years. Broader indices like the Philadelphia Semiconductor Index (SOX) are up 40% YTD, but rotation risks persist if AI hype cools.

Looking Ahead: Multi-Year Tailwinds

As August unfolds, eyes turn to Intel's earnings later this month and Nvidia's August 23 report. AMD's momentum suggests the AI chip wars are just starting. For investors, it's a high-stakes bet on compute demand outpacing supply. Macro resilience—cooling inflation, resilient consumer spending—supports the bull case.

In geopolitics, U.S. CHIPS Act subsidies ($52 billion) aim to onshore production, with AMD securing grants for New York fabs. This could mitigate Taiwan risks while fueling domestic growth.

AMD's Q2 triumph isn't just a quarterly win; it's a macro signal. AI is rearchitecting economies, from markets to supply chains. As Lisa Su put it, "The best is yet to come." For Global Insider readers tracking the intersection of tech, markets, and power, AMD's surge is must-watch.

Word count: 912